Today’s mortgage landscape offers some of the most attractive borrowing costs in recent years, with select lenders pushing 30-year fixed rates below 6%. The benchmark 30-year fixed purchase rate averages around 5.85% to 6.13% depending on the source, while refinance options hover slightly higher. Sub-6% deals represent a key threshold for many homeowners and buyers to act, especially as rates stabilize in the low-6% range amid cooling inflation signals and steady economic data. Shoppers who compare multiple offers can often secure rates well under the national averages reported by major surveys.

Mortgage and Refinance Rates Overview – February 15, 2026

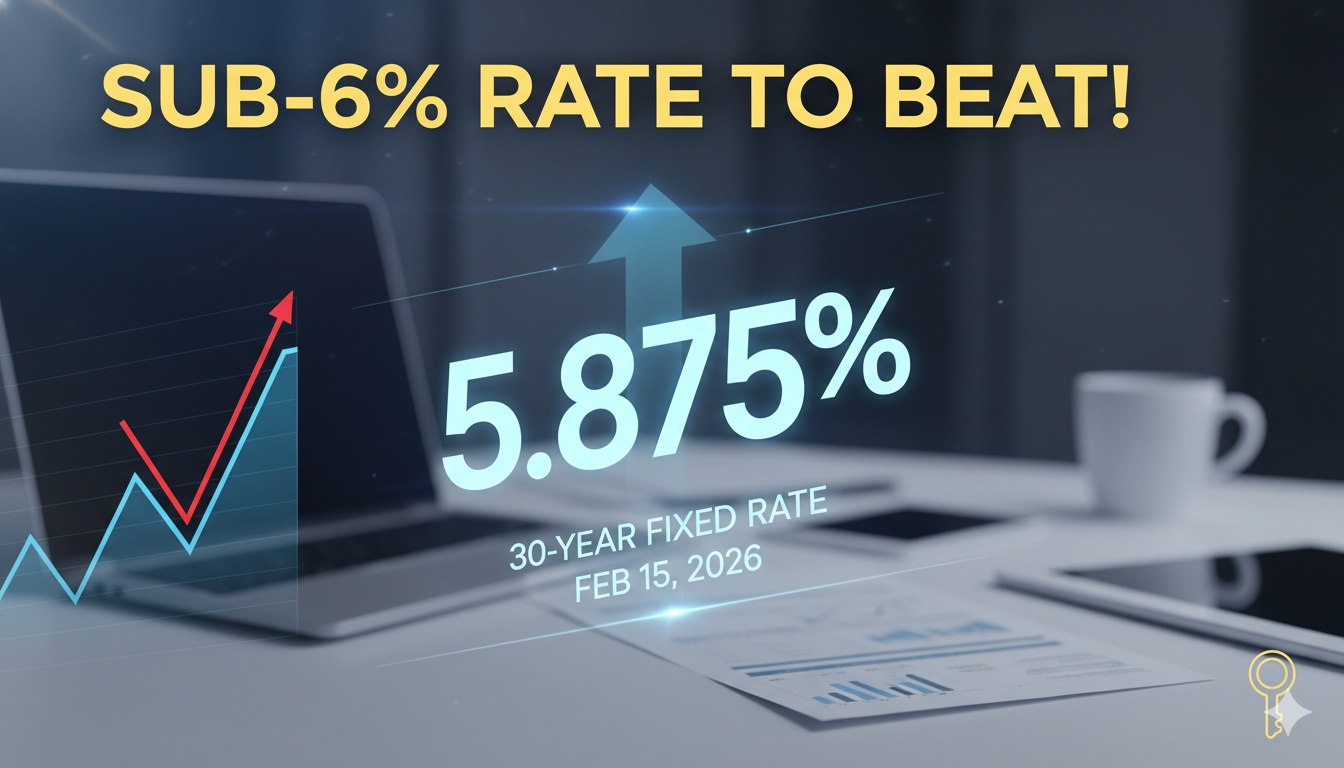

The mortgage market continues to deliver opportunities for both homebuyers and homeowners looking to refinance. As of mid-February 2026, the most competitive 30-year fixed mortgage rates have dipped into sub-6% territory at select lenders, making this a notable benchmark for borrowers. While official weekly surveys show the 30-year fixed at 6.09% (down slightly from the prior week), real-time lender marketplaces and daily averages reveal lower offers available to qualified applicants. This variance highlights the importance of shopping around—rates can differ by 0.25% or more based on credit profile, down payment, loan size, and lender competition.

For purchase loans, the standout sub-6% level on 30-year fixed products stands out as the rate to target. Borrowers with strong credit (typically 740+ FICO), solid debt-to-income ratios, and at least 20% down payment equity often qualify for these lower offers. Refinance rates tend to run 0.3% to 0.6% higher on average due to factors like seasoning requirements and closing cost structures, but motivated lenders are still advertising competitive terms to capture volume.

Current Average Mortgage Rates

Here are the latest national averages across major categories:

30-year fixed mortgage (purchase) : 5.85% to 6.13% (lender marketplace lows near 5.85%, broader averages around 6.13%)

30-year fixed refinance : 6.44% to 6.57%

15-year fixed mortgage : 5.26% to 5.51%

15-year fixed refinance : 5.88% to 5.96%

20-year fixed : Around 5.64% to 5.67%

5/1 ARM : 5.81% to 6.20%

7/1 ARM : 5.71% to 5.89%

These figures reflect a mix of daily lender data and broader surveys. The weekly Freddie Mac Primary Mortgage Market Survey (as of February 12, 2026) pegs the 30-year fixed at 6.09%, down 2 basis points from the previous week, and the 15-year at 5.44%, down 6 basis points. Year-over-year, rates remain significantly lower than the 6.87% seen in early 2025 for 30-year products.

Why Sub-6% 30-Year Fixed Rates Matter Right Now

The sub-6% mark on 30-year fixed loans has emerged as a psychological and practical tipping point for many in the housing market. When rates cross below this level, monthly payments become noticeably more manageable compared to higher thresholds. For example, on a $400,000 loan:

At 5.85%: Principal and interest payment ≈ $2,360/month

At 6.09%: ≈ $2,420/month (about $60 more per month)

At 6.50%: ≈ $2,528/month (over $160 more than sub-6%)

That monthly difference compounds over time, potentially saving tens of thousands in interest. For refinancers, dropping from a prior rate above 7% (common from 2023-2024 originations) into sub-6% territory can generate substantial long-term savings, often justifying closing costs within a few years.

Factors Driving Today’s Rates

Recent economic indicators have supported this stability in the low- to mid-6% range. Tame inflation readings, including a softer-than-expected January CPI, have eased pressure on bond yields that heavily influence mortgage pricing. The labor market remains resilient, but without aggressive overheating, allowing the Federal Reserve room to maintain a cautious stance on rate adjustments. Mortgage-backed securities demand and lender competition further contribute to the availability of sub-6% offers for top-tier borrowers.

Comparing Purchase vs. Refinance Options

Purchase borrowers generally access the lowest advertised rates due to streamlined underwriting and higher lender incentives for new originations. Refinancers face slightly elevated pricing, but those with significant equity or improved credit since origination can still find compelling deals.

Who Should Consider Locking In Now?

| Loan Type | Average Rate (Purchase) | Average Rate (Refinance) | Key Notes |

|---|---|---|---|

| 30-Year Fixed | 5.85% – 6.13% | 6.44% – 6.57% | Sub-6% achievable for strong profiles on purchase |

| 15-Year Fixed | 5.26% – 5.51% | 5.88% – 5.96% | Faster payoff, lower total interest |

| 5/1 ARM | 5.81% – 6.20% | Varies | Initial lower rate, but adjusts later |

| 7/1 ARM | 5.71% – 5.89% | Varies | Mid-term stability option |

Homebuyers eyeing spring inventory increases may benefit from securing a rate lock on sub-6% offers, especially if inventory remains tight. Refinancers with existing rates above 6.5%–7% should calculate break-even points—many can recoup costs in under 3–4 years at current levels. Those with adjustable-rate mortgages facing resets could also explore fixed-rate switches to lock in predictability.

Rates fluctuate daily based on market conditions, so borrowers should compare personalized quotes from multiple lenders to find the true sub-6% opportunities available today.

Disclaimer: This is for informational purposes only and does not constitute financial, legal, or investment advice. Mortgage rates are subject to change and vary by individual qualifications, location, and lender. Consult a qualified professional for personalized guidance.